Posts Tagged ‘Electricity’

PJM 2027/2028 Base Residual Auction Clears at Price Cap

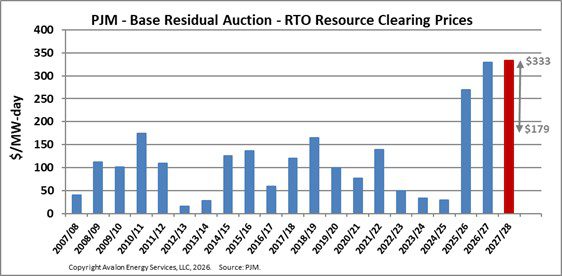

PJM 2027/2028 Base Residual Auction Clears at Price Cap In December 2025, PJM announced the results of its 2027/2028 Base Residual Auction (BRA), with the clearing price reaching the cap of $333.34/MW‑day across the RTO. In total, PJM procured 134,479 MW of Unforced Capacity (UCAP) through the auction. The graph below shows the history of…

Read More