Posts by Avalon Energy Services

PJM 2028/2029 Base Residual Auction Clears at Price Cap

PJM 2028/2029 Base Residual Auction Clears at Price Cap On July 14, 2026, PJM announced the results of its 2028/2029 Base Residual Auction (BRA), with the clearing price reaching the FERC approved price cap of $325/MW‑day across the RTO. In total, PJM procured 138,318 MW UCAP of generation and demand response resources through the auction with a resulting reserve…

Read MoreMaryland Electricity Imports

Maryland Electricity Imports Maryland generates roughly 60% of the electricity it consumes; the remaining 40% is imported from other PJM states. It is often assumed that these imports cost more than in‑state generation. That assumption is incorrect. In PJM, all generators—inside or outside Maryland—are paid the same locational marginal price (LMP) at a Maryland pricing…

Read MorePJM 2027/2028 Base Residual Auction Clears at Price Cap

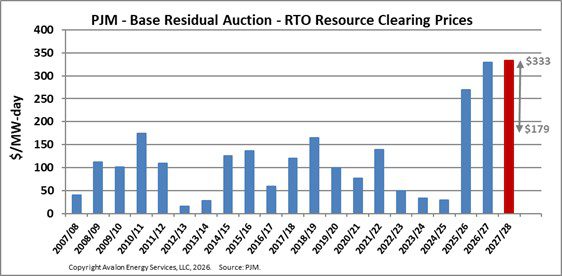

PJM 2027/2028 Base Residual Auction Clears at Price Cap In December 2025, PJM announced the results of its 2027/2028 Base Residual Auction (BRA), with the clearing price reaching the cap of $333.34/MW‑day across the RTO. In total, PJM procured 134,479 MW of Unforced Capacity (UCAP) through the auction. The graph below shows the history of…

Read More