Posts by Avalon Energy Services

Market Update

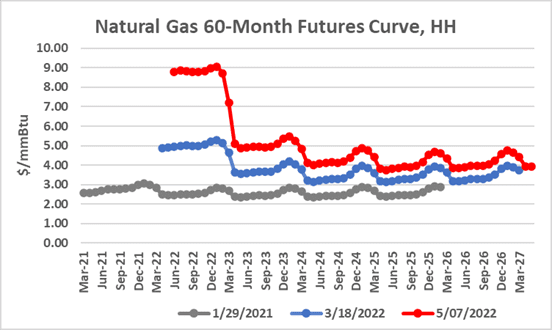

Market Update We looked at natural gas prices during mid-March compared to prices during the pandemic. The graph below plots forward natural gas prices at two points in time. The grey line represents the forward curve as of January 29, 2021 and the blue line as of March 18, 2022. It is important to note…

Read MoreWhat a Difference a Year Makes

What a Difference a Year Makes Last September, our COO, Jim McDonnell, was the lead-off speaker for the first session of the Maryland Clean Energy Center’s Energy Economy Speaker Series. The topic was State of the Sector: Impacts of Covid-19 on the Energy Economy. Jim provided a broad energy market update and then focused on…

Read MoreIn the News: Jim McDonnell Talks Energy Markets and Covid-19

By Evelyn Teel Our Chief Operating Officer, Jim McDonnell, was the lead-off speaker for the first session of the Maryland Clean Energy Center’s Energy Economy Speaker Series. The topic wasState of the Sector: Impacts of Covid-19 on the Energy Economy. Jim provided a broad energy market update and then focused on the differential impact of…

Read MoreEnergy Concepts: Power versus Energy

It is often tempting to use the words “power” and “energy” interchangeably. However, they are not, in fact, synonyms. In this blog post, we are going to share a brief explanation of the difference between the two. Fundamentally, power refers to a rate while energy refers to an amount. Power is a measure of energy…

Read MoreBuilding Ventilation and COVID-19

By Evelyn Teel COVID-19 has upended many facets of our lives, from where and how people work, to how children are educated, to how we socialize. As we try to find ways to get life back to normal, experts have been rethinking everything from the way schools are laid out to the way we order…

Read MoreAvalon Joins Virginia Chamber of Commerce

Avalon Energy Services is proud to announce that we are now members of the Virginia Chamber of Commerce. We also have joined the Corporate Sustainability and Environmental Executive Committee. As part of this group, we will contribute to the theory and practice of promoting business sustainability within Virginia. Whether in the form of systems and…

Read MoreThank You to Our Healthcare Heroes

By Evelyn Teel The COVID-19 pandemic has fundamentally altered the way we live. It has proven devastating for many people’s health and, most tragically, taken the lives of far too many. Frontline healthcare workers have faced incredible hurdles, preparing for and treating coronavirus patients, and potentially risked their own health to do so. The fallout…

Read MoreElectricity and Rock: Still Not Friends

By Evelyn Teel In a previous blog post, we discussed findings from the U.S. Geological Survey (USGS) that the I-95 corridor is particularly at risk of grid outages in the event of a geomagnetic storm. You can read that blog post here: https://avalonenergy.us/2018/07/electricity-meet-rock/. Further research has been conducted, and a new report from the USGS…

Read MoreDistributed Energy Resources Give You Options

By Evelyn Teel In the earliest days of electricity, generation happened close to where the electricity was used. A small hydro facility might have been used to power a single factory, or a coal-fired generator might have electrified a small town. As demand for electricity grew and we developed the capability to move it over…

Read MoreTrade-offs are Inevitable: Considerations for Our Energy System

By Evelyn Teel It is easy to think of energy as simply a commodity that makes our lives easier – by fueling our cars, keeping our homes comfortable, and powering our many devices. However, what if we sought to understand the more fundamental role energy plays in our lives? How would this reframe the conversation…

Read More